- Why Affordable Health Insurance Matters More Than Ever

- Understanding What “Affordable” Actually Means

- Types of Affordable Health Insurance Plans in India

- 1. Individual Health Insurance

- 2. Family Floater Plans

- 3. Government-Supported Schemes

- 4. Top-Up Plans

- Visualizing Health Insurance Choices

- Cost Comparison: What Affordable Plans Typically Look Like

- What Makes a Health Insurance Plan Truly Affordable?

- ✅ 1. Network Hospitals Near You

- ✅ 2. Low Waiting Periods

- ✅ 3. Minimal Co-Payment Clause

- ✅ 4. High Claim Settlement Ratio

- How to Buy Affordable Health Insurance Smartly (Not Emotionally)

- Step 1: Decide Coverage Before Looking at Price

- Step 2: Compare Premium vs Lifetime Cost

- Step 3: Use Deductibles Strategically

- Step 4: Buy Early, Not When You Need It

- The Biggest Myth: “I’m Healthy, I Don’t Need Insurance Yet”

- Key Features You Should Never Compromise On

- How Digital Platforms Have Made Health Insurance More Affordable

- Real-Life Example: A Middle-Class Family Scenario

- What to Avoid When Searching for Affordable Health Insurance India

- The Claim Process: Simpler Than Most People Think

- Affordable Health Insurance vs Medical Savings: Which Is Better?

- Tax Benefits Make Health Insurance Even More Affordable

- Final Thoughts: Affordable Doesn’t Mean Basic—It Means Smart

- ✅ Actionable Checklist Before You Buy

- 🚀 Call to Action

Affordable Health Insurance India: A Practical Guide to Getting Maximum Coverage Without Oversretching Your Budget

Healthcare costs in India are rising faster than most household incomes. A single hospitalization in a private hospital can wipe out years of savings. That’s why Affordable Health Insurance India is no longer a luxury—it’s a financial necessity.

But here’s the challenge: many people assume health insurance is expensive, complicated, or meant only for high-income families. In reality, India now offers a wide range of budget-friendly health insurance plans designed specifically for middle-class families, young professionals, and even students.

This guide breaks down how to find high-value yet affordable coverage, what features truly matter, and how to avoid overpaying while still protecting your health and finances.

Why Affordable Health Insurance Matters More Than Ever

In the past decade, India’s healthcare inflation has averaged 10–14% annually, significantly higher than general inflation. Even tier-2 cities like Tezpur, Guwahati, or Varanasi are seeing increasing private hospital costs.

Without insurance, families face three risks:

- Emergency Debt: Borrowing money during hospitalization

- Savings Erosion: Using education or retirement funds

- Delayed Treatment: Avoiding care due to cost concerns

Affordable insurance solves this by spreading risk across manageable premiums.

Understanding What “Affordable” Actually Means

Affordable doesn’t mean “cheapest.”

It means maximum protection at the lowest sustainable premium.

A good affordable plan should:

✔ Cover major hospitalization expenses

✔ Offer cashless treatment in nearby hospitals

✔ Include pre/post hospitalization costs

✔ Provide at least ₹5–10 lakh sum insured

✔ Keep premiums predictable over time

Types of Affordable Health Insurance Plans in India

1. Individual Health Insurance

Best for young professionals or single earners. Premiums are lower because risk is calculated per person.

2. Family Floater Plans

One sum insured shared across family members. These are often the most cost-effective option for Indian households.

3. Government-Supported Schemes

Schemes like Ayushman Bharat or state health programs provide subsidized coverage for eligible families.

4. Top-Up Plans

A smart trick to keep premiums low while increasing protection. You combine a base policy with a high-coverage top-up.

Visualizing Health Insurance Choices

4

These real-life scenarios show how insurance isn’t abstract—it directly affects decisions during emergencies.

Cost Comparison: What Affordable Plans Typically Look Like

| Age Group | Recommended Sum Insured | Avg. Annual Premium | Best Plan Type |

|---|---|---|---|

| 25–30 yrs | ₹5 lakh | ₹5,000–₹7,000 | Individual |

| 30–40 yrs | ₹10 lakh | ₹8,000–₹12,000 | Family Floater |

| 40–50 yrs | ₹10–15 lakh | ₹12,000–₹18,000 | Floater + Top-Up |

| 50+ yrs | ₹15 lakh+ | ₹18,000–₹28,000 | Comprehensive |

👉 Many people overestimate premiums—basic coverage often costs less than a smartphone EMI.

What Makes a Health Insurance Plan Truly Affordable?

✅ 1. Network Hospitals Near You

If cashless hospitals aren’t available in your city, even a cheap policy becomes expensive.

Always check:

- Local hospital availability

- Claim settlement partnerships

- Emergency accessibility

✅ 2. Low Waiting Periods

Affordable plans must still allow timely access to treatment. Look for:

- Pre-existing disease waiting period ≤ 3 years

- Maternity waiting period ≤ 2–3 years

✅ 3. Minimal Co-Payment Clause

Some cheap plans include hidden co-payments (you pay 20–30% of bills).

Avoid these unless premiums are dramatically lower.

✅ 4. High Claim Settlement Ratio

A plan is affordable only if it actually pays when needed.

How to Buy Affordable Health Insurance Smartly (Not Emotionally)

Many buyers choose based on advertisements or agent pressure. Instead, follow this 4-step method:

Step 1: Decide Coverage Before Looking at Price

Medical inflation means ₹3 lakh coverage is outdated.

Start with ₹5–10 lakh minimum.

Step 2: Compare Premium vs Lifetime Cost

A slightly higher premium today can prevent huge out-of-pocket costs later.

Step 3: Use Deductibles Strategically

Adding a deductible lowers premiums without sacrificing large coverage.

Step 4: Buy Early, Not When You Need It

Premiums increase sharply after age 35–40.

The Biggest Myth: “I’m Healthy, I Don’t Need Insurance Yet”

Young Indians delay insurance thinking:

“I’ll buy later.”

But here’s what actually happens:

| Buying Age | Premium | Waiting Period Impact |

|---|---|---|

| 26 yrs | Lowest | Cleared early |

| 35 yrs | +40% higher | Longer exclusions |

| 45 yrs | Almost double | Many restrictions |

Buying early is the single biggest affordability hack.

Key Features You Should Never Compromise On

Even budget plans should include:

- ✔ Cashless hospitalization

- ✔ Day-care procedures (modern treatments don’t require long stays)

- ✔ Pre & post hospitalization (30–60 days minimum)

- ✔ Ambulance charges

- ✔ Annual health check-ups

These features prevent hidden expenses.

How Digital Platforms Have Made Health Insurance More Affordable

The rise of online comparison tools has removed agent commissions, which used to inflate premiums.

Benefits of buying online:

- Transparent pricing

- Easy comparison

- No middleman cost

- Instant policy issuance

- Access to discounts

Digital-first insurers are driving the new affordability revolution in India.

Real-Life Example: A Middle-Class Family Scenario

Imagine a family of four in Assam:

- Parents aged 38 & 34

- Two children

- Combined income: ₹8–10 lakh/year

A ₹10 lakh floater policy may cost ₹10,000–₹13,000 annually.

That’s:

➡ Less than ₹35/day

➡ Cheaper than daily tea + snacks

➡ Protection against ₹3–5 lakh hospital bills

Insurance becomes a financial stabilizer, not an expense.

What to Avoid When Searching for Affordable Health Insurance India

❌ Choosing lowest premium without reading exclusions

❌ Ignoring room rent limits (this causes claim deductions)

❌ Buying too little coverage to “save money”

❌ Not disclosing medical history (claims may be rejected)

❌ Renewing late and losing continuity benefits

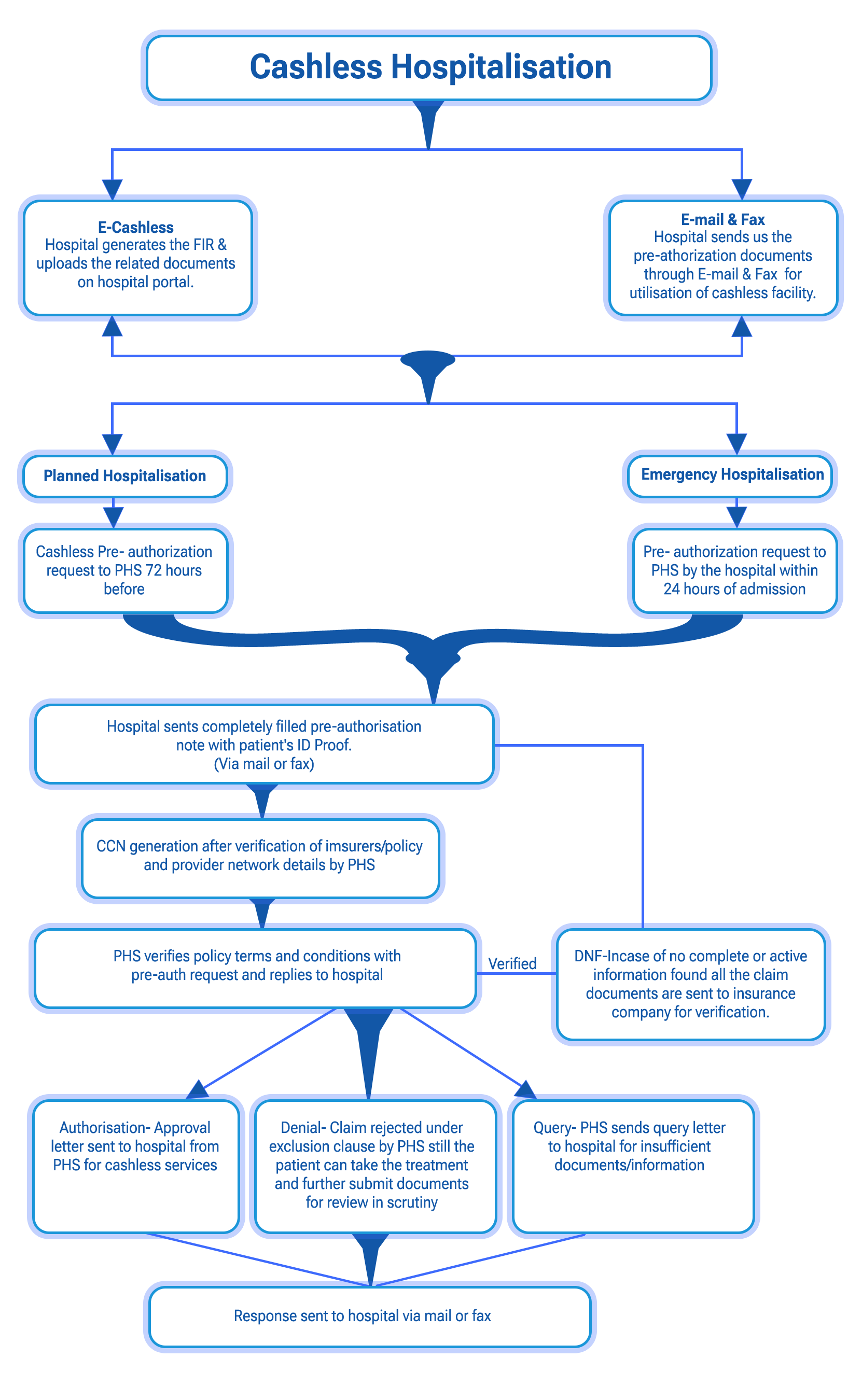

The Claim Process: Simpler Than Most People Think

4

Modern claim systems are streamlined:

- Show health card at hospital

- Insurance desk verifies details

- Treatment begins (cashless)

- Insurer settles bill directly

No running between offices, no emergency borrowing.

Affordable Health Insurance vs Medical Savings: Which Is Better?

Some people prefer saving money instead of buying insurance.

But mathematically:

| Strategy | 10-Year Savings | One Emergency Surgery |

|---|---|---|

| Self-saving ₹10k/year | ₹1 lakh | ₹3–5 lakh cost |

| Insurance ₹10k/year | Covered | Minimal out-of-pocket |

Insurance protects against uncertain, high-cost risks—something savings alone cannot do.

Tax Benefits Make Health Insurance Even More Affordable

Under Section 80D of the Income Tax Act:

- ₹25,000 deduction (self/family)

- ₹50,000 for senior citizen parents

This effectively reduces your real premium cost by 10–30% depending on your tax bracket.

Final Thoughts: Affordable Doesn’t Mean Basic—It Means Smart

The future of healthcare in India is uncertain, but one thing is clear:

Medical costs will continue rising.

Choosing Affordable Health Insurance India today is not about reacting to illness—it’s about building long-term financial resilience.

The smartest buyers are not the ones who pay the least.

They’re the ones who balance:

✔ Adequate coverage

✔ Reasonable premiums

✔ Long-term protection

✅ Actionable Checklist Before You Buy

- Compare at least 3 insurers

- Choose ₹5–10 lakh minimum coverage

- Verify nearby cashless hospitals

- Read exclusions carefully

- Buy before age 35 if possible

- Consider top-up plans for extra safety

🚀 Call to Action

If you haven’t reviewed your health coverage yet, now is the right time.

Take 20 minutes today to compare plans, calculate your needs, and secure a policy that protects both your health and your savings.

Your future self—and your family—will thank you for making this one smart financial decision.