- Why Medical Insurance in India Matters More Than Ever

- Types of Medical Insurance Plans Available in India

- 1. Individual Health Insurance

- 2. Family Floater Plans

- 3. Senior Citizen Health Insurance

- 4. Critical Illness Insurance

- 5. Top-Up & Super Top-Up Plans

- How Medical Insurance Actually Works (Beyond the Brochure)

- Two Ways Claims Are Settled

- Key Components You Must Understand

- Real Cost Comparison: With vs Without Medical Insurance

- Common Mistakes Indians Make While Buying Medical Insurance

- ❌ Choosing the Cheapest Plan

- ❌ Buying Too Late

- ❌ Ignoring Policy Wording

- ❌ Relying Only on Employer Insurance

- How Much Coverage Do You Actually Need?

- Unique Insight: Medical Insurance Is Also a Financial Planning Tool

- Features You Should Prioritize in 2026 Policies

- Look for These Smart Features

- Tax Benefits Under Medical Insurance India

- When Is the Best Time to Buy Medical Insurance?

- The Future of Medical Insurance in India

- Final Thoughts: Don’t Buy a Policy—Build Protection

- ✅ Action Step (CTA)

Medical Insurance India: A Practical Guide to Protecting Your Health & Wealth

Healthcare costs in India are rising faster than most people realize. A single hospitalization can wipe out years of savings. That’s why Medical Insurance India is no longer a luxury—it’s a financial survival tool.

Whether you are a salaried professional, self-employed, or building your career, the right medical insurance policy ensures that a health emergency doesn’t turn into a financial crisis.

This guide goes beyond definitions. It explains how medical insurance actually works in real life, what most people misunderstand, and how you can choose wisely.

Why Medical Insurance in India Matters More Than Ever

India’s healthcare system offers world-class treatment—but often at high out-of-pocket costs. Unlike countries with universal coverage, individuals here bear a significant share of medical expenses.

Key realities driving the need for coverage:

- Lifestyle diseases are increasing at younger ages

- Private hospital costs are rising 10–15% annually

- Emergency treatments require instant liquidity

- Savings alone cannot handle critical illnesses

- Tax benefits encourage long-term planning

Medical insurance acts as a financial shield, ensuring treatment decisions are based on medical need—not affordability.

Types of Medical Insurance Plans Available in India

4

Understanding plan types is essential before choosing coverage. Many buyers select policies blindly based on premium instead of suitability.

1. Individual Health Insurance

Covers one person with a dedicated sum insured.

Best For:

Young professionals, individuals with specific health risks.

2. Family Floater Plans

One sum insured shared by the entire family.

Best For:

Married couples, young families seeking affordability.

3. Senior Citizen Health Insurance

Designed for people aged 60+, with coverage for age-related conditions.

4. Critical Illness Insurance

Provides a lump sum payout upon diagnosis of serious diseases like cancer, stroke, or heart attack.

5. Top-Up & Super Top-Up Plans

Extra coverage activated after a deductible limit—ideal for increasing protection at low cost.

How Medical Insurance Actually Works (Beyond the Brochure)

4

Many people think insurance simply “pays hospital bills.” The mechanism is more structured.

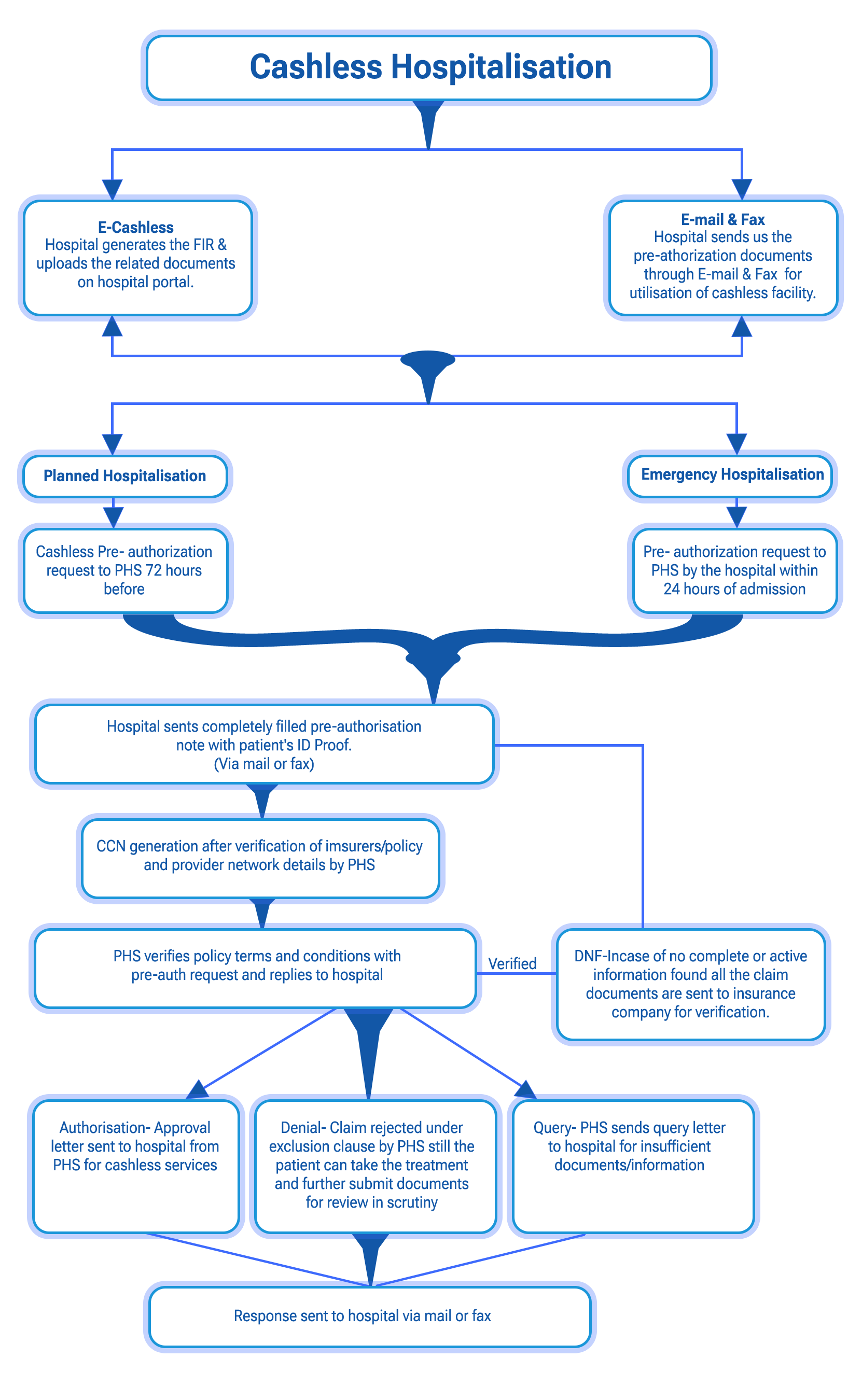

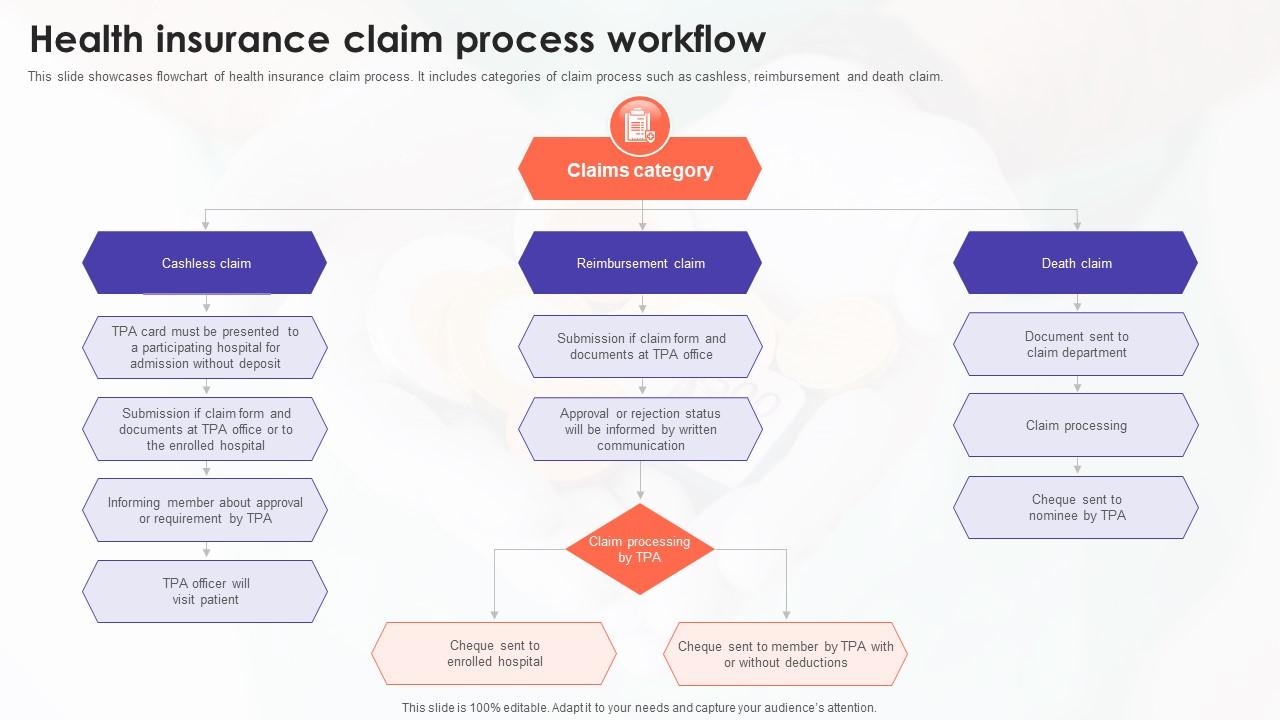

Two Ways Claims Are Settled

| Claim Type | How It Works | When It’s Used |

|---|---|---|

| Cashless Claim | Insurer pays hospital directly | Network hospitals |

| Reimbursement | You pay first, insurer refunds | Non-network hospitals |

Key Components You Must Understand

- Sum Insured: Maximum amount insurer will pay annually

- Premium: Yearly cost of maintaining policy

- Waiting Period: Time before certain illnesses are covered

- Co-payment: Portion you must pay from your pocket

- Network Hospitals: Hospitals tied to insurer for cashless treatment

Ignoring these details leads to claim rejections—not lack of insurance.

Real Cost Comparison: With vs Without Medical Insurance

Let’s look at a realistic hospitalization scenario.

| Treatment Type | Average Cost Without Insurance | Cost With Insurance |

|---|---|---|

| Appendix Surgery | ₹1.5 – ₹2.5 lakh | Mostly covered |

| Heart Angioplasty | ₹3 – ₹5 lakh | Paid by insurer |

| Cancer Treatment | ₹8 – ₹15 lakh | Covered as per plan |

| ICU Stay (3 days) | ₹1 lakh+ | Cashless possible |

This is why Medical Insurance India is fundamentally about protecting long-term wealth—not saving tax.

Common Mistakes Indians Make While Buying Medical Insurance

❌ Choosing the Cheapest Plan

Low premiums often mean:

- Low coverage limits

- High co-payment

- Room rent restrictions

❌ Buying Too Late

Insurance after age 40 becomes:

- Expensive

- Restricted by waiting periods

- Harder to approve

❌ Ignoring Policy Wording

Most claim disputes happen because buyers never read:

- Exclusions

- Sub-limits

- Disease-specific clauses

❌ Relying Only on Employer Insurance

Corporate coverage ends when:

- You change jobs

- You retire

- Company alters benefits

Personal insurance ensures continuity.

How Much Coverage Do You Actually Need?

A practical formula:

👉 Minimum Coverage = 50% of your annual income × 10

But in metro or tier-2 cities, experts recommend:

- Individuals: ₹10–15 lakh cover

- Families: ₹20–25 lakh floater

- With super top-up: ₹50 lakh protection

Medical inflation makes small policies obsolete within 5–7 years.

Unique Insight: Medical Insurance Is Also a Financial Planning Tool

People think of insurance as an expense. In reality, it functions like:

- Emergency fund protector

- Retirement savings shield

- Wealth preservation strategy

- Tax optimization instrument

Without insurance, one medical emergency can derail decades of financial discipline.

Features You Should Prioritize in 2026 Policies

4

Modern medical insurance in India now includes value-added benefits beyond hospitalization.

Look for These Smart Features

✔ Cashless treatment in large hospital networks

✔ No-Claim Bonus (coverage increases every year)

✔ Free annual health checkups

✔ Day-care procedure coverage (no 24-hour admission needed)

✔ Pre- and post-hospitalization expenses

✔ Restoration benefit (sum insured refills automatically)

These features transform insurance from reactive protection to proactive healthcare management.

Tax Benefits Under Medical Insurance India

Medical insurance also reduces tax liability under Section 80D:

| Category | Deduction Allowed |

|---|---|

| Self & Family | Up to ₹25,000 |

| Parents (<60 yrs) | ₹25,000 extra |

| Senior Citizen Parents | ₹50,000 extra |

So you are not just protecting health—you’re optimizing taxes legally.

When Is the Best Time to Buy Medical Insurance?

Answer: Before you think you need it.

Buying young gives you:

- Lower premiums locked for life

- Coverage before illnesses develop

- Zero waiting-period stress later

- Higher cumulative bonuses

Insurance is cheapest when you are healthiest—and most expensive when you are not.

The Future of Medical Insurance in India

Healthcare and technology are merging rapidly. Expect:

- AI-based premium personalization

- App-based instant claims

- Preventive care rewards

- Wearable-linked wellness discounts

- OPD and mental health integration

Medical insurance is evolving from “sickness coverage” to “lifestyle protection.”

Final Thoughts: Don’t Buy a Policy—Build Protection

Medical Insurance India is not about ticking a financial checkbox.

It is about ensuring:

- Your family never delays treatment

- Your savings remain intact

- Your future goals stay on track

- A medical crisis doesn’t become a financial one

The right policy gives something priceless: peace of mind.

✅ Action Step (CTA)

If you haven’t reviewed your medical coverage recently, now is the time.

✔ Evaluate your current sum insured

✔ Compare whether it matches today’s healthcare costs

✔ Upgrade with a top-up if needed

✔ Start early if you haven’t bought insurance yet

Your health is unpredictable. Your financial protection shouldn’t be.

If you’d like, I can also create:

- A comparison article of Top Medical Insurance Providers in India

- A YouTube script based on this blog

- A downloadable checklist for choosing the right policy